The used car market has changed dramatically over the past few years. What once felt like a straightforward transaction has now become a minefield of hidden risks and financial uncertainty.

In 2026, buying a car from a private seller is no longer as simple as shaking hands and exchanging keys. The world has shifted in ways that put everyday buyers at serious disadvantage.

More buyers are turning to private listings to avoid dealership markups and negotiation pressure. The appeal is obvious lower prices, direct communication, and the chance to find a great deal hidden in someone’s driveway.

However, the dangers lurking beneath the surface have multiplied significantly in recent years. Fraud, deception, and legal gaps have made private car buying one of the riskiest financial decisions you can make today.

Cybercrime targeting vehicle transactions has surged to record levels. Title fraud has become more sophisticated and harder to detect than ever before.

Mechanical deception is increasingly difficult to spot as modern cars rely on complex software that can mask serious problems. Consumer protection laws that apply to dealerships simply do not extend to private sales.

Whether you are browsing local classifieds or scrolling through online marketplaces, the risks are real and costly. Understanding these dangers before you hand over your money could save you from a devastating financial mistake. Here are five critical reasons why buying a car from a private seller is riskier than ever in 2026.

No Legal Consumer Protections or Warranties

When you walk into a dealership and purchase a vehicle, the law stands firmly behind you. There are multiple layers of consumer protection designed to ensure that what you buy is exactly what you were promised.

Private sellers operate in an entirely different legal universe. One where your rights as a buyer are severely limited and often completely nonexistent.

In most countries and states, dealerships are legally required to provide a minimum warranty period on used vehicles. This means if your car breaks down shortly after purchase, you have clear legal recourse to demand a repair or a full refund.

Private sellers are almost universally protected by the principle of “sold as is.” This single phrase strips you of nearly every legal remedy the moment you sign the paperwork.

“Sold as is” is one of the most powerful legal shields available to any seller. It means the seller bears absolutely no responsibility for any defect, fault, or failure discovered after the sale is complete.

Even if the car breaks down on your drive home from the purchase, you have no legal claim against the seller. In most jurisdictions, the courts will simply uphold the “sold as is” agreement you unknowingly accepted.

Consumer protection agencies like the FTC in the United States have full jurisdiction over licensed dealers. These agencies can investigate complaints, impose heavy fines, and force refunds when dealers act dishonestly or mislead buyers.

Private sellers fall completely outside the authority of these agencies. This leaves you with no government body to turn to when things go wrong after the transaction.

The absence of warranty protection is particularly dangerous in 2026. Modern vehicles are extraordinarily complex machines packed with advanced driver assistance systems, onboard computers, and interconnected electronic networks.

A fault in any one of these systems can cost thousands of dollars to diagnose and repair. Without warranty protection, every single one of those costs falls entirely on your shoulders from day one.

Legal experts consistently warn that private car purchase disputes are among the hardest cases to win in small claims court. Unless you can prove deliberate and documented fraud, judges almost always side with the seller due to the “sold as is” clause.

Many buyers are shocked to discover how little protection they actually have. By the time they realize the car has serious problems, their money is long gone with no practical way to get it back.

In 2026, with vehicle repair costs at an all-time high due to supply chain pressures and parts shortages, this lack of protection is more dangerous than ever. A single unexpected repair bill can easily wipe out any savings you made by avoiding a dealership in the first place.

Dealerships are also required by law to disclose known defects before a sale. Private sellers have no such obligation in many places, meaning they can legally stay silent about problems they are fully aware of.

The bottom line is brutally simple. When you buy from a private seller, you are taking on 100 percent of the financial and legal risk with virtually zero safety net beneath you.

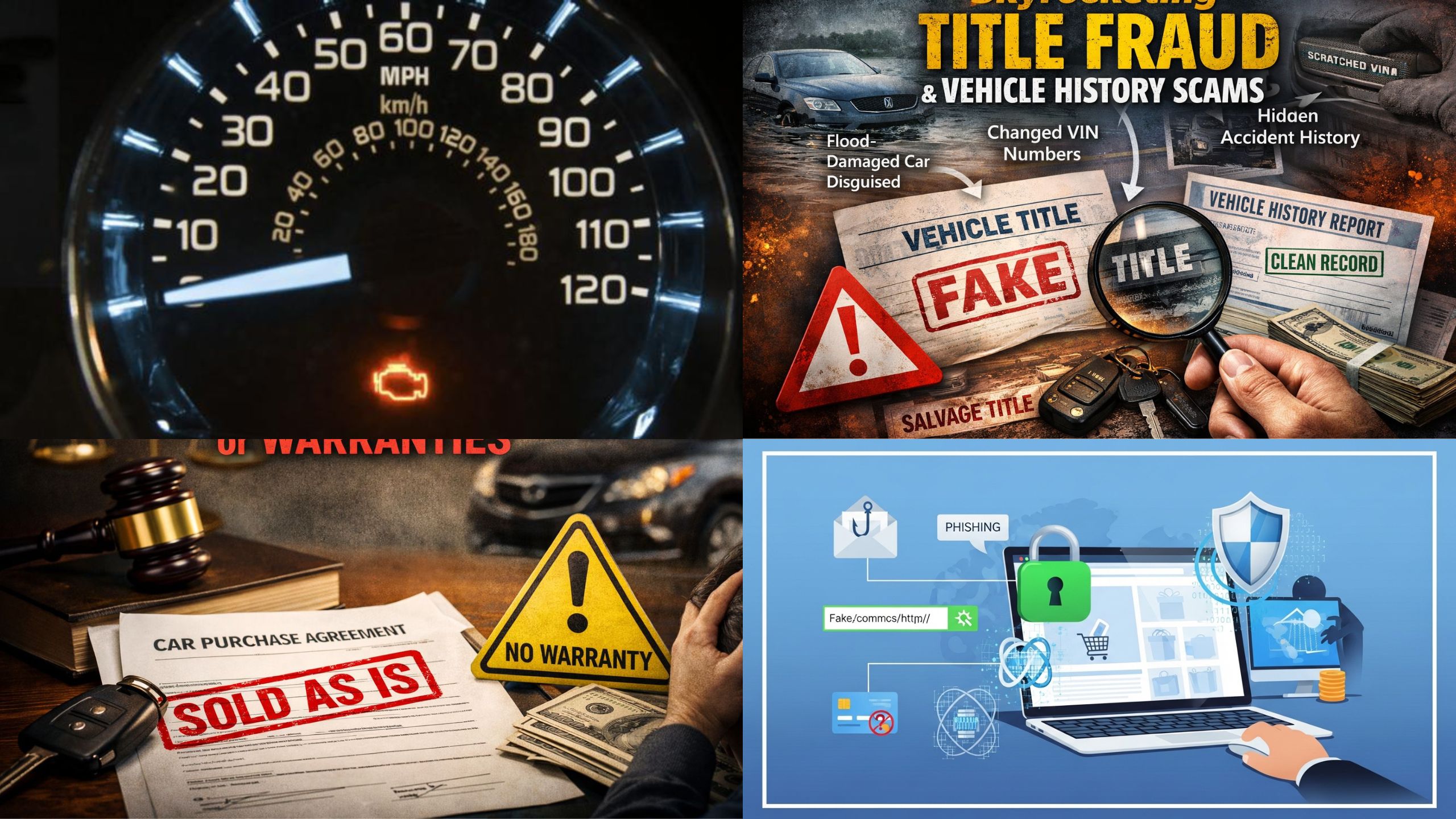

Skyrocketing Title Fraud and Vehicle History Scams

Title fraud was already a growing problem before 2026. But advancements in document forgery technology and the rise of sophisticated online scammers have pushed this issue to alarming new levels.

A vehicle title is the single most important document in any car transaction. It proves legal ownership and reveals critical information about the car’s financial and legal history.

Forging a title document has become disturbingly easy for criminals. High-quality desktop printing technology and widely available editing software have made fake titles nearly indistinguishable from genuine ones to the untrained eye.

Private sellers are under no obligation to use certified or notarized title transfer processes in many states. This creates a dangerous gap that fraudsters exploit aggressively and repeatedly.

One of the most dangerous forms of title fraud is title washing. This is the illegal practice of moving a vehicle across state or country lines to erase a salvage, flood, or rebuilt title designation from its official records.

A car that was totaled in a flood in one state can reappear with a clean title in another state just weeks later. The buyer sees a clean document and has absolutely no reason to suspect the vehicle has a dark and destructive history.

Flood-damaged vehicles are particularly common in the used car market following the increased frequency of extreme weather events. These cars often look perfectly fine on the outside but carry hidden corrosion, mold, and electrical damage that causes catastrophic failure months later.

Vehicle history report services like Carfax have become more popular but are far from foolproof. Many private sellers know exactly how to structure a sale in a way that keeps damaging information off these reports entirely.

Odometer fraud is another massive and growing problem in private sales. Rolling back a digital odometer has become easier with widely available OBD port tools that anyone can purchase cheaply online.

A car showing 60,000 miles on the dashboard might actually have 160,000 miles of real wear on its engine and components. You would be paying a high price for a vehicle that is already well past its reliable service life.

In 2026, artificial intelligence tools have made it even easier to create convincing fake maintenance records and service histories. A private seller can hand you a beautifully formatted document showing years of perfect maintenance that never actually happened.

Stolen vehicle sales through private channels have also increased significantly. Criminal networks have become more adept at creating clean-looking paperwork for vehicles that are actually stolen property.

If you unknowingly purchase a stolen vehicle from a private seller, the consequences fall on you. The car can be seized by law enforcement without compensation, leaving you with no vehicle and no money.

The safest approach is always to run a comprehensive title check through official government databases before handing over any payment. However, many buyers skip this step entirely when they are excited about a deal, and private sellers often pressure buyers to decide quickly before the opportunity disappears.

In a dealership environment, these checks are mandatory and legally enforced. In a private sale, they are entirely your responsibility and entirely your risk if you get them wrong.

Also Read: 10 Engines That Can Handle Standard Grade Fuel Without Losing Longevity

Hidden Mechanical Problems Disguised by Modern Technology

Buying a used car from a private seller has always carried mechanical risk. But in 2026, that risk has reached a completely new and frightening level thanks to the complexity of modern vehicle technology.

Modern cars are essentially computers on wheels. They contain dozens of electronic control units managing everything from engine performance and braking systems to climate control and entertainment features.

These systems communicate through a central network that can be manipulated in ways the average buyer would never detect. A knowledgeable seller can temporarily suppress warning lights and fault codes before a sale using inexpensive diagnostic tools.

When you test drive the vehicle, everything appears perfectly normal. The dashboard shows no warning lights and the car drives smoothly, but serious faults are quietly hiding in the background waiting to surface after you drive away.

This practice is known informally as “code clearing” and it is completely invisible to a standard visual inspection. Within days or weeks of the purchase, the original fault codes return and the problems become impossible to ignore.

Modern engines also respond very differently cold versus warm. A seller who knows their engine has a serious issue will always ensure the car is fully warmed up before you arrive for a test drive, masking startup problems that would otherwise be immediately obvious.

Transmission problems are among the most expensive repairs a car owner can face. These issues often only appear under specific driving conditions such as highway speeds or when towing, conditions you would never test during a brief private sale test drive.

Structural damage from previous accidents is another hidden danger. A vehicle can appear visually perfect after a professional cosmetic repair while hiding bent frame components that compromise safety and handling.

Advanced computer diagnostics at a professional shop can cost between $100 and $300. Many buyers consider this an unnecessary expense when they are already trying to save money on the purchase, and many private sellers actively discourage professional inspections.

A seller who resists or refuses a pre-purchase inspection should be treated as an immediate red flag. Yet many buyers are so excited about the price or the car itself that they overlook this critical warning sign.

Battery degradation in electric and hybrid vehicles is one of the most significant hidden mechanical risks in 2026. The used EV market has expanded enormously, and battery health is something most buyers have no way to accurately assess without specialized equipment.

An electric vehicle battery pack can cost anywhere from $8,000 to $20,000 to replace depending on the model. A private seller has every incentive to hide declining battery health and almost no obligation to disclose it honestly.

Rust is another problem that skilled sellers know how to hide temporarily using spray coatings and cosmetic treatments. Surface rust that has penetrated structural components can be completely invisible during a casual inspection in a driveway.

The financial consequences of discovering hidden mechanical problems after a private sale are devastating. You have already paid for the car and you have almost no legal means of recovering your money when serious faults emerge days later.

Professional mechanics consistently advise that no private car purchase should ever be completed without a full pre-purchase inspection at an independent shop. Yet thousands of buyers skip this step every single day and pay a very heavy price for doing so.

Rising Online Scams and Digital Payment Fraud

The way people buy and sell cars has been transformed by digital technology over the past decade. In 2026, the majority of private car listings begin online, and this shift has opened the door to an entirely new category of sophisticated financial fraud.

Online car scams have evolved far beyond the obvious fake listings of the early internet era. Today’s fraudsters use professional-quality photographs, convincing vehicle history reports, and even fake video calls to create an illusion of complete legitimacy.

One of the most common scams targeting private car buyers involves sellers who claim to be located overseas due to military service or a work assignment. They offer the car at a below-market price and ask for a deposit to hold the vehicle until they can arrange shipping to your location.

The deposit disappears immediately and the seller vanishes completely. The car never existed in the first place, and the entire elaborate story was constructed purely to steal your money.

Escrow fraud is another rapidly growing scam in the private car market. A fraudster directs you to a fake escrow website that looks completely professional and legitimate but is entirely controlled by the criminal operation.

You transfer your payment to what you believe is a secure third-party account. In reality, the money goes directly into the scammer’s pocket and the website disappears within days.

Deepfake technology has added a frightening new dimension to online car fraud in 2026. Scammers can now conduct convincing video calls using AI-generated faces, making it appear as though you are speaking with a real and trustworthy person.

You believe you are building a genuine relationship with the seller and establishing trust. In reality, you are communicating with a sophisticated artificial intelligence system programmed to steal your money.

Payment reversal scams also trap many private car buyers each year. A scammer appears to overpay you or sends a payment through a method that can be disputed or reversed after you have already handed over the vehicle or a deposit.

By the time the original payment is reversed by the bank, both the money and the scammer have completely disappeared. You are left with a financial loss and no practical means of recovery.

Cryptocurrency payment requests in private car sales should always be treated as a major warning sign. Digital currencies offer criminals complete anonymity and make it virtually impossible to trace or recover stolen funds.

In 2026, digital payment fraud targeting car buyers costs victims collectively hundreds of millions of dollars annually. Law enforcement agencies consistently report that car sale fraud is among the most difficult categories of financial crime to investigate and prosecute.

The anonymity of online platforms means you often know almost nothing real about the person you are dealing with. Profile information, reviews, and even photographs can all be fabricated with minimal effort using tools that are freely available online.

Even transactions that begin as genuine can turn fraudulent at the final stage. A legitimate seller can be replaced by a scammer who intercepts communication and redirects payment to a different account right at the moment of closing the deal.

Protecting yourself requires extreme caution, extensive verification, and insistence on in-person transactions with traceable payment methods. However, the level of sophistication shown by modern car sale fraudsters makes even cautious buyers vulnerable to losing significant amounts of money.

Financing Complications and Undisclosed Financial Encumbrances

One of the most financially devastating risks of buying a car from a private seller in 2026 is the very real possibility of purchasing a vehicle that still has an outstanding loan, lien, or financial encumbrance attached to it. This single issue has ruined thousands of buyers financially and it remains dangerously common.

When a vehicle has an outstanding finance agreement, the lender holds a legal interest in that car. This interest does not disappear simply because the seller has transferred the keys and title to you.

The lender retains the legal right to repossess the vehicle regardless of the fact that you paid the private seller in good faith. You can lose the car completely without receiving a single penny of compensation.

This situation is far more common than most buyers realize. Many private sellers are in financial difficulty and are attempting to sell a car they do not actually have the legal right to sell without the lender’s involvement and approval.

Some sellers are entirely unaware that their vehicle has a lien attached to it. Others know perfectly well and choose to conceal this critical information because disclosing it would kill the sale immediately.

Checking for outstanding finance is technically possible through various services and official databases. However, these checks are not universally mandatory in private sales and many buyers simply do not know they need to perform them.

In 2026, with personal debt levels at record highs in many countries, the proportion of privately sold vehicles with outstanding finance has increased considerably. More people are selling cars they are still paying for and hoping the buyer never discovers the problem until it is too late.

Mechanics liens are another form of financial encumbrance that buyers rarely consider. If a previous owner had work done on the vehicle and failed to pay the repair shop, the shop may hold a legal claim against that vehicle.

This claim travels with the car regardless of how many times it changes ownership. You could find yourself facing legal action from a repair shop over a debt you had absolutely nothing to do with.

Property tax liens in certain states can also attach to vehicles. Outstanding taxes owed by a previous owner can become your legal problem the moment you take ownership of the vehicle.

The process of clearing an encumbered title after purchase is extremely costly, time consuming, and stressful. Legal fees alone can quickly exceed the savings you made by choosing a private sale over a dealership purchase.

Dealerships are legally required to deliver a vehicle with a clean and unencumbered title as a standard part of every transaction. This protection alone is worth a significant premium over what you might pay in a private sale.

Even when private sellers are acting in complete good faith, they may not fully understand the financial obligations attached to their own vehicle. Ignorance is not a legal defense for you as the buyer when the consequences come calling.

Some buyers have found themselves making payments on a vehicle loan while simultaneously dealing with repossession proceedings initiated by the original lender. This nightmarish scenario is entirely avoidable but only if you know to look for it before completing the purchase.

Financing your own purchase of a privately sold vehicle adds yet another layer of complication. Many mainstream lenders are increasingly reluctant to finance private sale purchases precisely because the risk profile is so much higher than a dealership transaction.

You may find yourself limited to higher interest rate financing options or forced to use personal loans with unfavorable terms. The total cost of the vehicle over time ends up significantly higher than it would have been through a structured dealership arrangement.

The financial encumbrance risk is compounding in 2026 because economic pressures are pushing more distressed vehicle owners into the private sale market. The very sellers offering the most attractive prices are often doing so precisely because they are in financial trouble with obligations attached to the car.

A deal that looks too good to be true in the private sale market almost always is. The price discount you are being offered frequently exists because the seller knows there is a problem with the vehicle’s financial status that they are hoping you will not discover in time.

Also Read: 10 Cars With Such High Resale Value That Buying Used Is a Mistake