Choosing between leasing and buying a car is one of the most important financial decisions many individuals face, especially when planning long-term transportation costs.

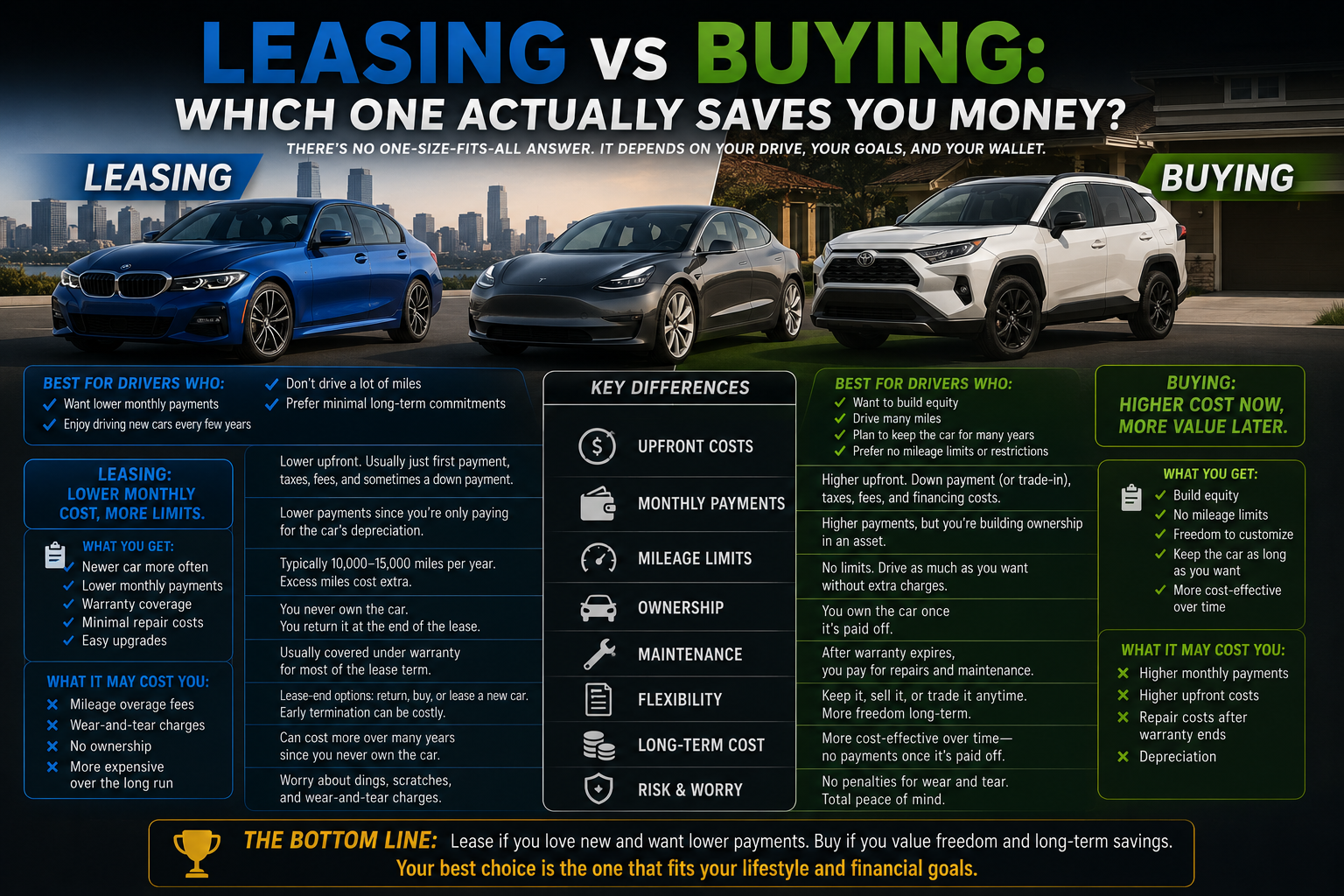

At first glance, both options may seem similar because they allow you to drive a vehicle without paying the full price upfront, but the financial structure behind each option is very different. Leasing a car is essentially a long-term rental agreement where you pay for the use of the vehicle over a fixed period, usually two to four years, after which you return it or sometimes buy it at a predetermined price.

Buying a car, on the other hand, means you are purchasing the vehicle either outright or through a loan, giving you full ownership once the loan is fully repaid. The decision between leasing and buying affects monthly budgets, long-term wealth building, maintenance responsibilities, and even lifestyle flexibility.

People often get attracted to leasing because of lower monthly payments and the appeal of driving a new car every few years, while others prefer buying because it leads to ownership and potential long-term savings.

However, the real answer to which option saves more money depends on several factors, such as how long you plan to keep the car, how many miles you drive each year, how well you maintain vehicles, and how you value ownership versus convenience.

In many cases, leasing may seem cheaper in the short term but can become more expensive over a long period due to continuous payments with no asset accumulation. Buying may require higher upfront or monthly costs, but it builds equity and can reduce transportation expenses significantly once the loan is paid off.

Additionally, factors like depreciation, interest rates, insurance differences, and repair costs play a major role in determining the financial impact. Understanding these differences is essential before making a commitment, because a car is not just a mode of transport but also a significant financial liability or asset depending on how it is acquired.

This article will break down leasing versus buying in detail, comparing costs, long-term value, hidden expenses, and practical scenarios so you can clearly understand which option aligns better with your financial goals and driving habits.

Also Read: 10 Electric Vehicles That Spend the Least Time at Charging Stations

Understanding Leasing and Buying

Leasing and buying are often discussed as if they are simple variations of the same concept, but in reality, they function in fundamentally different ways. Leasing is structured around usage rather than ownership. When you lease a vehicle, you are essentially paying for the depreciation that occurs during the period you use the car, along with interest charges and fees set by the leasing company.

The car is returned at the end of the term unless you choose a buyout option. This structure makes leasing appealing for people who prioritize lower monthly payments and driving newer models frequently. It also reduces concerns about long-term maintenance, since most leased vehicles remain under warranty during the lease period.

Buying, however, is centered on ownership and long-term value accumulation. When you purchase a vehicle through financing or an upfront payment, you are building equity in the asset. Over time, once the loan is paid off, the car becomes fully yours, and your only remaining costs are maintenance, insurance, and fuel.

Unlike leasing, there are no restrictions on customization or mileage, which gives owners more freedom in how they use the vehicle. The tradeoff is that monthly payments tend to be higher in the early years, and the buyer assumes responsibility for depreciation and resale value.

One important distinction lies in how each option treats long-term financial planning. Leasing keeps drivers in a continuous cycle of payments without ownership accumulation, which can be manageable for those who prefer predictable costs but less beneficial for wealth building.

Buying creates a long-term asset that can be sold or traded later, often recovering a portion of the investment. This difference becomes more significant over time, especially for individuals who plan to keep their vehicle for many years.

Leasing can feel easier because it avoids the commitment of long-term ownership and reduces worries about repair costs outside warranty coverage. Buying, however, appeals to those who value control, stability, and long-term savings. Understanding these structural differences is essential before comparing actual costs.

Also Read: 10 Reasons Cars Got Smaller Over the Last 60 Years

The Upfront Costs Compared

One of the most noticeable differences between leasing and buying is the initial financial requirement. Leasing typically requires a lower upfront payment, often consisting of the first month’s payment, a security deposit in some cases, registration fees, and acquisition fees.

This makes leasing more accessible for individuals who may not have large savings available for a down payment. It also allows drivers to get into newer vehicles without a significant financial barrier.

Buying a car, on the other hand, usually requires a higher upfront cost if you want favorable loan terms. While it is possible to purchase a car with little or no down payment, doing so often results in higher monthly payments and increased interest costs over time.

A substantial down payment, typically ranging from ten to twenty percent, helps reduce the loan burden and interest paid. This makes buying more capital-intensive at the beginning but more cost-efficient in the long run.

One factor influencing upfront costs is insurance. Leased vehicles often require comprehensive insurance coverage with higher liability limits because the leasing company retains ownership of the car.

This can increase monthly insurance premiums compared to owning an older or fully paid-off vehicle. Buyers may have more flexibility in adjusting coverage once the car is older or fully paid off.

Taxes and fees also differ between the two options depending on local regulations. In many regions, leasing allows individuals to pay tax only on the monthly payment rather than the full value of the vehicle, which reduces the immediate financial burden. Buyers typically pay sales tax on the full purchase price upfront or as part of financing, which increases initial expenses.

Leasing minimizes upfront financial pressure, while buying requires more initial investment but leads to ownership. This tradeoff is central to understanding which option may be more suitable depending on financial readiness and long-term planning.

")

The Long-Term Financial Impact

When evaluating leasing versus buying from a long-term financial perspective, the differences become significantly more pronounced. Leasing can appear affordable month to month, but it does not create any lasting financial value.

At the end of each lease term, the driver must either return the vehicle or enter a new lease, which effectively restarts the payment cycle. Over ten or fifteen years, this can result in continuous payments without ever owning a vehicle, making leasing more expensive in the long run for many users.

Buying a car introduces depreciation as a key financial factor. Vehicles lose value over time, often most rapidly in the first few years. However, once a car loan is fully paid off, the owner benefits from years of usage without monthly payments, aside from maintenance and insurance.

This creates a period where transportation costs are significantly reduced compared to leasing. The longer a person keeps a vehicle after paying off the loan, the more cost-effective buying becomes.

Interest rates also play a role in long-term cost differences. Auto loans involve interest payments, which increase the total cost of ownership. However, these costs are finite, unlike leasing, where payments continue indefinitely. Even if a buyer pays more initially, they eventually reach a point where they are no longer making payments, which can lead to substantial savings over time.

Leased vehicles are often newer and covered by warranty, reducing repair expenses during the lease period. However, these costs are effectively built into the lease pricing. Buyers of older vehicles may face higher maintenance expenses, but this is often offset by the absence of monthly payments once the loan is complete.

In most long-term scenarios, buying tends to be more financially efficient, especially for individuals who keep vehicles for many years. Leasing is better suited for those who prioritize short-term affordability and frequent upgrades rather than long-term savings.

Also Read: 10 Reasons Cars Got Smaller Over the Last 60 Years

Which Option Is Best for Different Types of Drivers

The decision between leasing and buying is not universal, and the best choice depends heavily on driving habits, financial stability, and personal preferences. For individuals who enjoy driving new cars every few years and prefer predictable monthly expenses, leasing can be an attractive option.

It eliminates concerns about resale value and reduces exposure to long-term maintenance risks. This makes it suitable for professionals who prioritize convenience and image over ownership.

For high-mileage drivers, buying is generally more practical. Leasing agreements often include mileage limits, and exceeding those limits results in additional charges that can quickly become expensive.

Buyers do not face these restrictions, making ownership more flexible for people who travel long distances regularly or use their vehicles for commuting or business purposes.

Financial discipline also plays a major role. Individuals who prefer structured budgeting and long-term asset building often benefit more from buying. Once the loan is paid off, they gain a valuable asset and reduce monthly obligations. On the other hand, those who prefer lower immediate costs and do not want to commit to long-term ownership may find leasing easier to manage.

Lifestyle preferences also influence the decision. People who value having the latest technology, safety features, and design updates may prefer leasing since it allows frequent upgrades. Meanwhile, those who are comfortable keeping a vehicle for many years and maximizing its value tend to favor buying.

Leasing suits flexibility and convenience, while buying supports long-term savings and ownership. The right choice depends on balancing financial priorities with lifestyle expectations.

Frequently Asked Questions

Many people have similar questions when comparing leasing and buying, especially when trying to understand hidden costs and long-term implications. One common question is whether leasing is always cheaper than buying. The answer is no. Leasing usually has lower monthly payments, but it does not build equity, which means long-term costs can be higher.

Is buying a car always the best financial decision? While buying is generally more cost-effective over many years, it depends on how long the vehicle is kept and how well it is maintained. Short-term ownership may not always deliver significant savings compared to leasing.

People also ask about maintenance costs. Leased vehicles often have lower out-of-pocket repair expenses due to warranty coverage, while owned vehicles may require more maintenance over time, especially as they age. However, once a car loan is paid off, maintenance becomes the primary expense, which is often still lower than leasing payments.

When buying a car, resale value can offset some of the initial cost, but it varies widely depending on the brand, model, and condition. Leasing removes this concern entirely since the vehicle is returned at the end of the term.

Many wonder which option is better for long-term wealth building. Buying is generally more favorable because it leads to ownership of a depreciating but usable asset, while leasing is better suited for short-term convenience rather than financial growth.