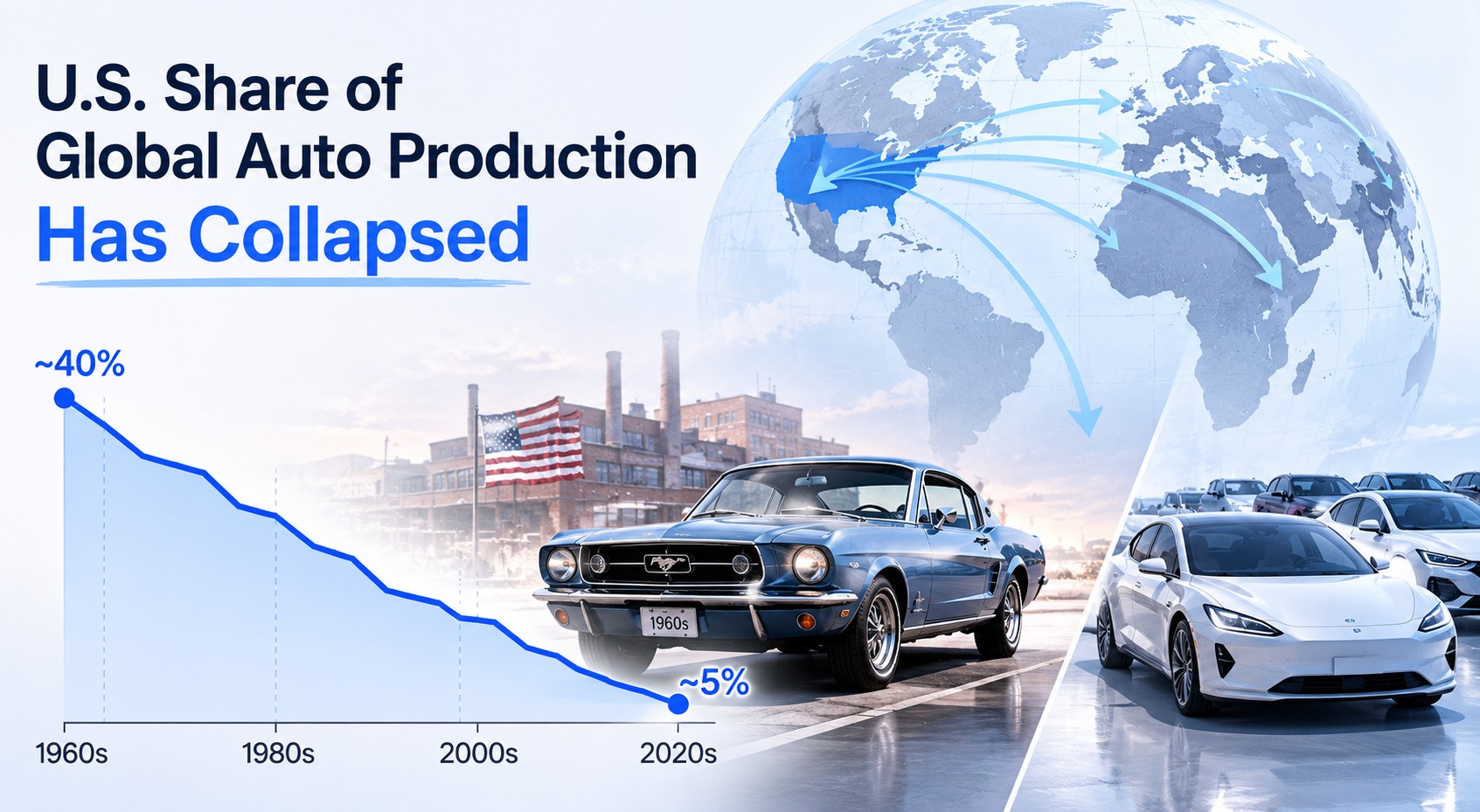

The American automobile industry was once the undisputed king of global manufacturing. In the early 1960s, the United States produced nearly half of all the cars built anywhere worldwide. Detroit was not just a city, it was a symbol of industrial dominance, economic strength, and national pride.

The “Big Three” automakers, General Motors, Ford, and Chrysler, ruled the global market with an iron grip. Their factories employed millions of workers and powered entire regional economies across the Midwest.

But that era of unchallenged supremacy is long gone. Today, the United States accounts for only around 12 to 15 percent of global automobile production.

China alone now builds more cars in a single year than the US has produced in many recent decades combined. Japan, Germany, South Korea, and India have all carved out massive shares of the market.

The collapse is not merely statistical it reflects deeper shifts in technology, labor, trade policy, and global competition. Understanding how America fell from producing nearly half the world’s cars to a relatively modest share is a story of complacency, transformation, and fierce international rivalry. It is a story that still shapes economic and political debates in the United States today.

The Golden Era and the Seeds of Decline

America’s automotive dominance in the 1950s and early 1960s was staggering. The US produced roughly 8 million vehicles annually while the rest of the world was still rebuilding from World War II.

Detroit’s automakers operated with little serious competition from abroad. Domestic consumers had high incomes, wide roads, and a deep cultural love affair with the automobile.

The Big Three grew enormous and, in many ways, complacent. They focused on large, fuel-hungry vehicles with high profit margins rather than investing in fuel efficiency or engineering innovation. Management structures became bloated and slow to adapt to changing consumer preferences.

The first serious cracks appeared in the late 1960s and early 1970s. Japan was quietly building a disciplined, efficient, and quality-focused auto industry. German manufacturers like Volkswagen were already finding success in the US market with smaller, reliable vehicles.

The 1973 OPEC oil embargo delivered a brutal shock. American consumers suddenly wanted fuel-efficient cars that Detroit was poorly positioned to provide. Japanese automakers like Toyota and Honda stepped into the gap with remarkable speed and efficiency.

Meanwhile, American factories were burdened by high labor costs and rigid union contracts. The productivity gap between US and Japanese assembly lines became embarrassingly wide during this period. Japan was applying lean manufacturing principles that American companies were slow to adopt.

By the late 1970s, the structural decline was clearly underway. The US share of global production had already dropped significantly, and the industry had not yet seen its worst years. What had been a manufacturing paradise was becoming a warning story about industrial overconfidence.

Globalization, Foreign Competition, and Industry Restructuring

The 1980s brought a wave of foreign competition that permanently reshaped the American auto world. Japanese manufacturers began building plants directly on American soil, the so-called “transplants,” to avoid import restrictions. Honda opened its Ohio plant in 1982, followed by Toyota, Nissan, and others in quick succession.

These foreign-owned plants were highly efficient and produced vehicles American consumers increasingly preferred. They drew talent and investment away from traditional Detroit strongholds in Michigan and Ohio. The competitive pressure was enormous and relentless.

General Motors, Ford, and Chrysler fought back with mixed results. They formed joint ventures, adopted some Japanese manufacturing techniques, and lobbied hard for trade protections. But they could never fully close the quality and efficiency gap that had opened during the 1970s.

The 1990s saw further globalization as automakers shifted production to lower-cost countries. Mexico became a major production hub for American brands under NAFTA. South Korea emerged as a serious competitor with Hyundai and Kia building globally competitive vehicles at lower price points.

The 2008 financial crisis nearly destroyed what remained of domestic US auto manufacturing. General Motors and Chrysler required massive government bailouts to survive.

The crisis exposed decades of structural weaknesses, pension obligations, and unsustainable business models that had been papered over during profitable years.

The US auto industry did recover, largely through painful restructuring and government intervention. But recovery did not mean restoration of the old dominance.

The global production map had been permanently redrawn. America was now just one important player among many in a fiercely competitive worldwide industry.

The Rise of China and the Electric Vehicle Revolution

No development has more dramatically altered the global auto industry than China’s rise. China surpassed the United States as the world’s largest auto producer around 2008 and has never looked back. Today, China produces roughly 25 to 30 million vehicles annually, more than double America’s output.

Chinese automakers initially built low-cost vehicles for domestic consumption. But they have rapidly upgraded their capabilities, particularly in electric vehicles, where companies like BYD are now genuinely world-class competitors. The transition to EVs has given China a chance to leapfrog legacy Western manufacturers entirely.

The electric vehicle revolution presents both an opportunity and an existential challenge for the US industry. American companies like Tesla have shown that the US can lead in EV innovation. But traditional automakers are struggling to transition their massive legacy manufacturing operations fast enough.

Government policy is now central to the competitive battle. The Inflation Reduction Act introduced significant incentives to boost domestic EV production and battery manufacturing. Trade tariffs on Chinese vehicles reflect the geopolitical dimension that auto competition has now acquired.

The stakes are enormous. Automobiles and their supply chains represent millions of jobs and hundreds of billions in economic output. Whether the US can rebuild a stronger share of global production in the EV era remains genuinely uncertain. The 1960s dominance will never return, but the fight for the future of automotive manufacturing is only just beginning.